After two years of declining funding activity, biotech venture capital offered signs of a rebound in 2024. However, investor patterns have changed, with VCs favoring high-profile companies.

KEY TAKEAWAYS

- After two years of post-pandemic decline—marked by high inflation, rising rates and geopolitical instability—stronger venture capital activity in 2024 signalled what may look like a recovery for biotech funding.

- VCs are becoming increasingly picky, concentrating larger investments on fewer high-profile biotech with experienced teams, strong scientific data, targeting validated markets—raising the bar for smaller, innovative startups seeking funding.

- Series A rounds dominated biotech funding in 2024, capturing six of the ten largest deals and driving Series A median deal sizes sharply upward, reflecting VCs' preference for early-stage companies with strong fundamentals.

- Oncology and immunology remain top funding targets, together capturing over half of VC investments, while metabolism emerged as a trending therapeutic area, tripling its funding share thanks to breakthroughs in GLP-1 therapies.

- Small molecules held steady, representing a third of global VC funding, while antibodies and peptides, driven by GLP-1 breakthroughs, emerged as major biotech growth areas.

Signs of a recovery for biotech VC funding

The pandemic sugar rush brought a peak in VC funding, leading many early-stage biotech to go public with inflated valuations. This resulted in overvalued biotech failing to deliver milestones, triggering a decline in investor confidence.

At the same time, high inflation, rising interest rates, and geopolitical instability added further pressure. A harsher financial climate which led VCs to prioritize portfolio triage and, in turn, to a slowdown in capital deployment over the past two years.

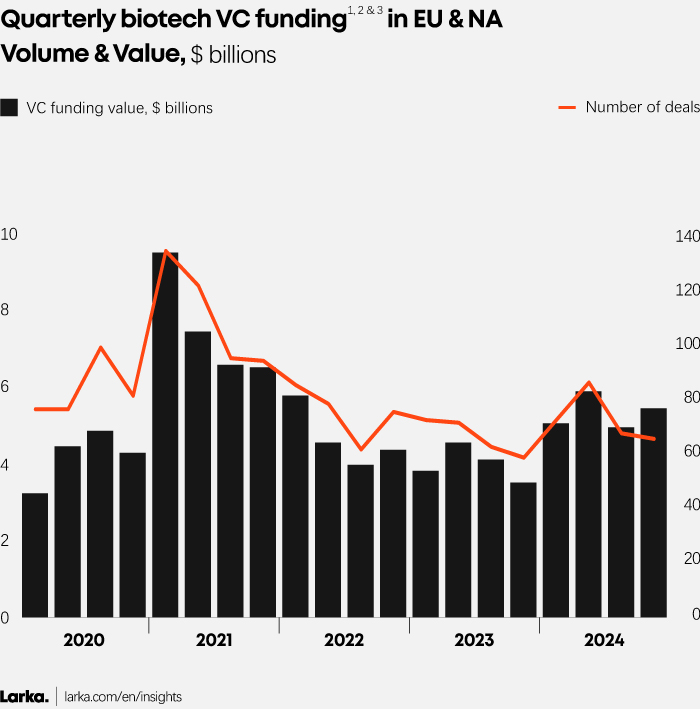

However, 2024 was marked with stronger venture capital activity, as well as increased M&A dealmaking and IPOs—signalling what looks like a turnaround and renewed confidence in the biotech sector (Figure 1).

Figure 1

1. VC funding focusing on pharma drugs (excluding diagnostic, medical device, pure play technological platform etc.).

2. Includes all type of Series—i.e. Series Seed, A, B, C+, extension, etc.

3. If the Series amount was not disclosed, it was conservatively estimated based on the types of funding rounds raised.

The much anticipated funding recovery might have come true in 2024, as venture capitalists regained their appetite for biotech.

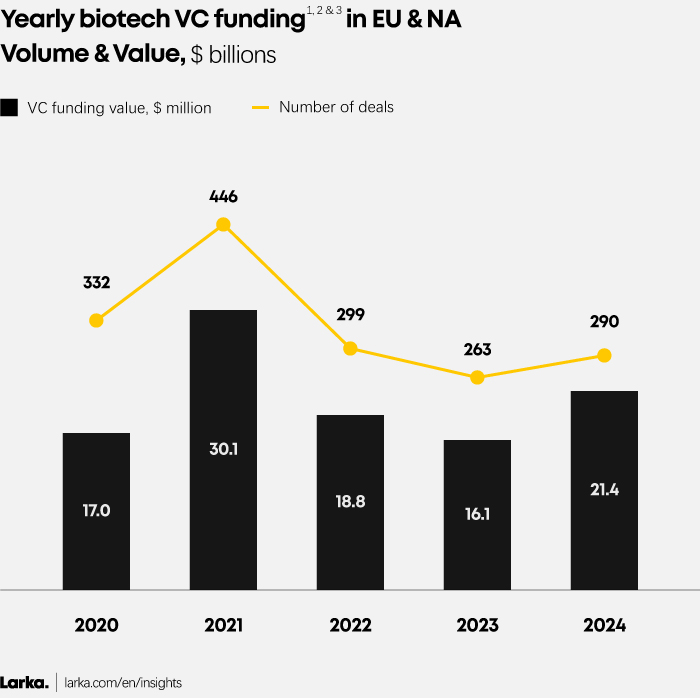

For the first time since 2021, total VC funding increased year-over-year, reaching $21.4 billion versus $16.1 billion in 2023—surpassing pre-pandemic levels (Figure 2). Furthermore, 2024 recorded the strongest quarters since early 2022, with VC funding consistently remaining above $5 billion in total funding value (Figure 1).

Figure 2

1. VC funding focusing on pharma drugs (excluding diagnostic, medical device, pure play technological platform etc.).

2. Includes all type of Series—i.e. Series Seed, A, B, C+, extension, etc.

3. If the Series amount was not disclosed, it was conservatively estimated based on the types of funding rounds raised.

VCs double down on high-quality biotech

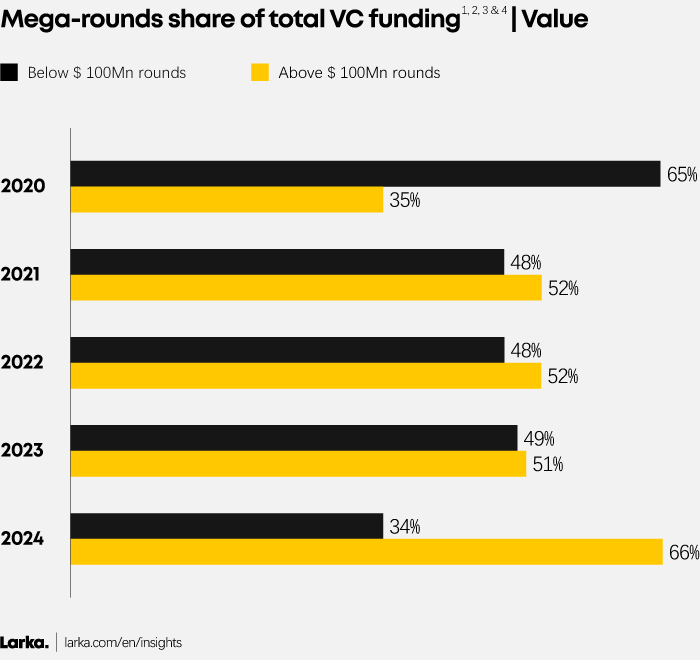

The biotech funding uptick has been fueled by larger deals and mega-rounds—financings exceeding $100 million—rather than a broad recovery across the sector.

While the number of deals has declined by 13% since 2020, total deal value has grown by 26%, signalling a fundamental shift in how capital is being deployed (See Figure 2).

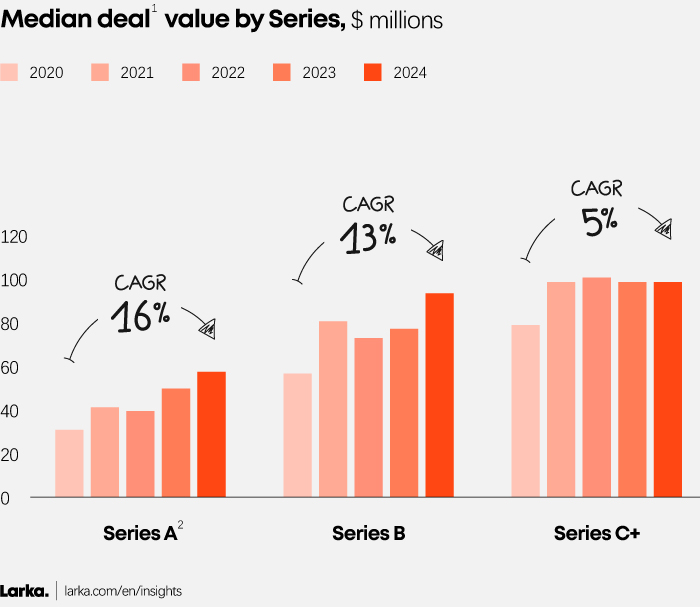

Mega-rounds have flipped their share of total VC funding from 35% pre-pandemic to 66% in 2024, reflecting a more concentrated investment strategy favouring high-value deals (See Figure 3). This concentration is also highlighted in the consistent increase in median deal value across all funding Series (See Figure 4).

Figure 3

1. VC funding focusing on pharma drugs (excluding diagnostic, medical device, pure play technological platform etc.).

2. VC funding focusing on Europe and North America—excluding Asia and ROW.

3. Includes all type of Series—i.e. Series Seed, A, B, C+, extension, etc.

4. If the Series amount was not disclosed, it was conservatively estimated based on the types of funding rounds raised.

This shift in investment pattern is concentrating dollars on fewer, high-profile biotech companies with experienced leadership teams, strong scientific data, or those operating in large, well-validated markets such as oncology, immunology and metabolism—the top three indications among 2024’s 10 largest financings (See Figure 5).

With investors adopting a more selective approach to de-risk portfolios and improve capital efficiency, access to capital is becoming more challenging for innovative start-ups operating in emerging areas—as they need to tick more boxes to attract VC.

Figure 4

1. Series extension are excluded.

2. Series A exclude Series Seed.

Figure 5

1. VC funding focusing on pharma drugs (excluding diagnostic, medical device, pure play technological platform etc.).

2. Includes all type of Series—i.e. Series Seed, A, B, C+, extension, etc.

3. If the Series amount was not disclosed, it was conservatively estimated based on the types of funding rounds raised.

Abbreviations – SM: Small Molecules; Rec. Prot.: Recombinant Proteins; CGT: Cell & Gene Therapy; Immuno.: Immunology; Gen. Diseases: Genetic Diseases.

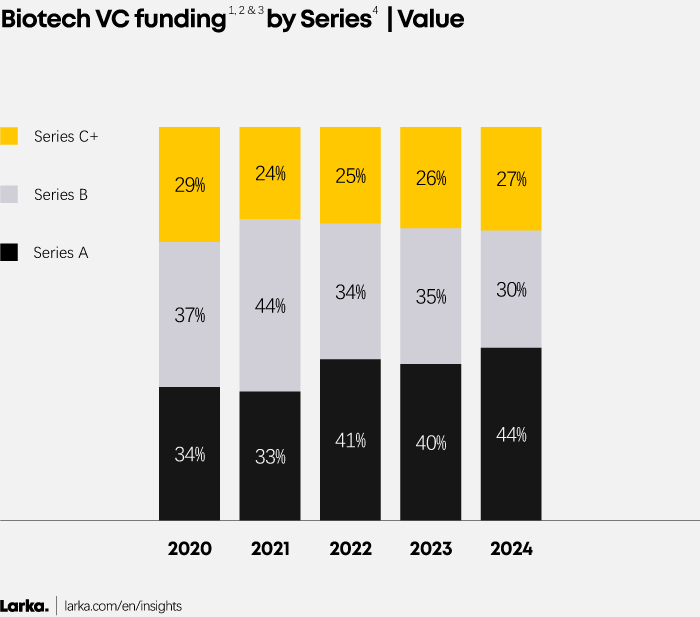

Series A dominate the funding landscape

Investors now raise the bar higher, yet they are eager to bet big on early-stage biotech if they have strong fundamentals.

Series A rounds dominated in 2024. Accounting for six of the ten largest financings—versus 1 in 2020, 2 in 2021-2022, and 4 in 2023—with an average deal size of $ 344Mn (see Figure 5). Notably, all the top 10 biotech companies were US-based.

This dominance of early-stage deals is also reflected in the growing Series A share of total VC funding value, up from 34% to 44% in five years (Figure 6). At the same time, the Series A median deal size surged, soaring from $32.5 million to $58.7 million over the past five years (Figure 4).

Figure 6

1. VC funding focusing on pharma drugs (excluding diagnostic, medical device, pure play technological platform etc.).

2. VC funding focusing on Europe and North America—excluding Asia and ROW.

3. If the Series amount was not disclosed, it was conservatively estimated based on the types of funding rounds raised.

4. Series A include Series Seed, Seed extension and A extension. Series B include Series B and B extension. Series C include Series C, C extension, D and beyond. Please note that if no information was provided regarding the type of series, we decided to estimate it based on the amount and the potential previous rounds raised by the biotech.

Oncology and immunology led the way, funding in metabolism tripled

Oncology and immunology are still driving the market and together account for more than half of the dollars invested by venture capitalists. Notably, immunology’s share of VC funding has nearly doubled in the past five years (Figure 7).

This strong focus in oncology and immunology is driven by unmet medical needs and high growth potential. Oncology remains pharma’s top revenue driver, supported by a large patient pool and rising cancer incidence, making it a key target for investment and innovation.

Figure 7

1. VC funding focusing on pharma drugs (excluding diagnostic, medical device, pure play technological platform etc.).

2. VC funding focusing on Europe and North America—excluding Asia and ROW.

3. Includes all type of Series—i.e. Series Seed, A, B, C+, extension, etc.

4. The value allocation by therapeutic area (TA) has been calculated by dividing the total funding amount ($) for a biotech company by the number of TA present in its pipeline.

5. Other includes cardiovascular, ophthalmology, psychiatry, etc.

While the shares of neurology and genetic diseases declined between 2020 and 2024, metabolism tripled its share of funding value, emerging as the new trending therapeutic area (Figure 7).

Recent advancements in GLP-1 therapies and the commercialization of drugs like Ozempic (Novo Nordisk) and Mounjaro (Eli Lilly)—originally developed for diabetes but now widely used for weight loss—have propelled metabolism into one of the most trending therapeutic areas.

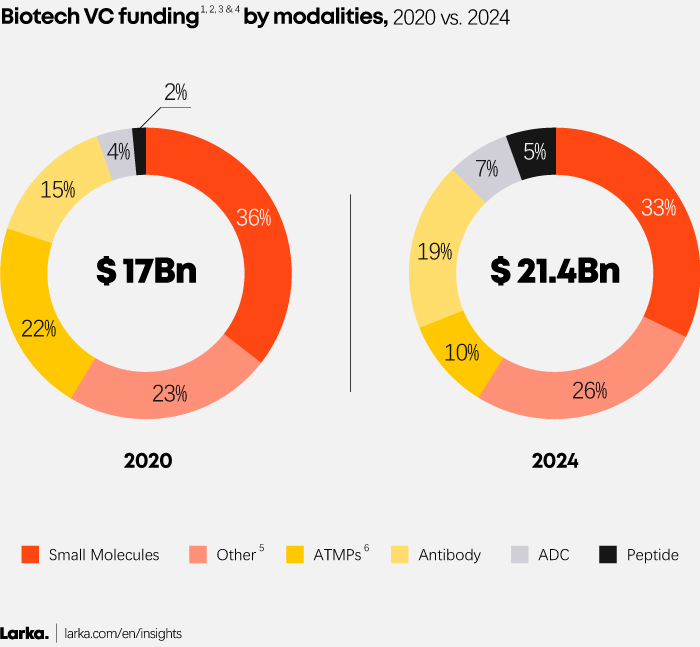

Small Molecules Hold Strong, Antibodies and Peptides Gain Momentum

Small molecules continue to play a major role in biotech fundraising, accounting for a third of global VC investments in 2024, largely due to their ability to address a wide range of therapeutic areas.

Figure 8

1. VC funding focusing on pharma drugs (excl. diagnostic, medical device, etc.).

2. VC funding focusing on Europe and North America—excluding Asia and ROW.

3. Includes all type of Series—i.e. Series Seed, A, B, C+, extension, etc.

4. The value allocation by modality has been calculated by dividing the total funding amount ($) for a biotech company by the number of modalities present in its pipeline.

5. Other includes oligonucleotides, radiotherapeutics, recombinant protein (excl. antibody), mRNA, plasmid, oncolytic viruses, LBP-Microbiota and other undisclosed modalities.

6. ATMPs include cell and gene therapy, cell therapy and gene therapy.

Interest in ATMPs has waned over the past year, meanwhile antibodies and ADCs are gaining traction. Monoclonal antibodies (mAbs) remain a key player in oncology and immunology while expanding into other serious diseases. Beyond their well-established presence, mAbs are driving continuous innovation, with bispecific antibodies emerging as a promising new class of biologics with significant therapeutic potential.

Another modality on the rise is peptides, fueled by breakthroughs in GLP-1 therapies. Their versatility in targeting diabetes and weight management has opened a massive market opportunity, making peptides a key trend to watch.

An optimistic outlook for the biopharma ecosystem in 2025

Early signs suggest this recovery could extend into 2025. Our latest data shows January marked the strongest start of a year since 2021 with total VC dollars hitting $3.1 billion—nearly double the same month last year—fueled by a dozen of mega-rounds, including Verdiva Bio’s $ 411Mn Series A and Kardigan’s $ 300Mn Series A.

With rate cuts expected throughout 2025 in the US and Europe, funding and IPO markets could maintain a strong momentum. As the cost of capital falls, investments will become more attractive—particularly in high-risk, long-term sectors like biotech. With traditionally “safe” investments offering lower yields, VCs may increasingly shift towards higher-risk, high-reward opportunities, creating a more favourable environment for early-stage biotech startups.

However, this scenario has yet to materialize, as deal volumes in 2024 remained below 2020 and 2022 levels. To stay ahead and attract funding, biotech companies will still need to think strategically and adapt to investors’ higher expectations.

Our 2024 survey of 50+ leading venture capitalists identified eight key factors biotech companies must prioritize to secure funding—insights we anticipate will continue to shape VC’s investment decisions in 2025:

- Innovative science

- Strong scientific data

- Experienced management team

- Market potential

- Robust supply chain

- Regulatory strategy

- Intellectual Property

- Financial health and projections

With the biotech funding landscape regaining traction and cash runways stabilizing, biotech may soon shift from cash-preservation mode back to more traditional spending patterns with pharma services and suppliers that focus on preclinical and clinical segments. Meanwhile, pharma services and suppliers will need to develop commercial strategy that enables high-end customers acquisition—as transaction volumes remain lower.

Coupled with improving economic conditions and expected rate cuts, this anticipated surge in demand for pharma services and suppliers could translate into increased Private Equity activity in this sector throughout 2025—signalling brighter prospects for the broader biopharma ecosystem.