Building on our recent analysis of Big Pharma’s M&A strategies in 2024, this report delves into the latest drug modality and therapeutic area trends—based on our monitoring of each year’s Top 10 Pharma companies M&A activity, from 2019 to 1H24.

Read more about this report’s methodology.

KEY TAKEAWAYS

- Despite a transitory slowdown in large oncology deals during the pandemic, the oncology market remained Big Pharma’s favourite overall—backed by steady interest in smaller deals targeting innovative technologies.

- Accounting for 46% of Top 10 Pharma acquisitions over the past five years, Small Molecule (SM) drugs are still a major theme—driven by their versatility across therapeutic areas and emerging innovations.

- Representing over a third of M&A deals during 2019-1H24, antibody-based assets including mAbs and ADCs are going strong.

- Top 10 Pharma’s interest in ADC has sky-rocketed driven by their strong efficacy, safety, and expanding applications beyond oncology, reflected in major recent acquisitions.

- The pandemic spurred M&A activity in vaccines, mRNA, and immunology, driven by their scalability, broad potential, and the vital role of the immune system in severe COVID-19 cases.

- M&A interest in metabolic diseases surged in 2023, driven by the potential of GLP-1 receptor agonists, with notable deals like Roche and Sanofi’s $2.9 billion acquisition of Carmot Therapeutics.

- Radiopharmaceuticals gained momentum in 1H24 as a promising alternative to traditional radiation therapy, highlighted by major deals like BMS’s $4.1 billion acquisition of RayzeBio and AstraZeneca’s $2.4 billion deal for Fusion Pharmaceuticals.

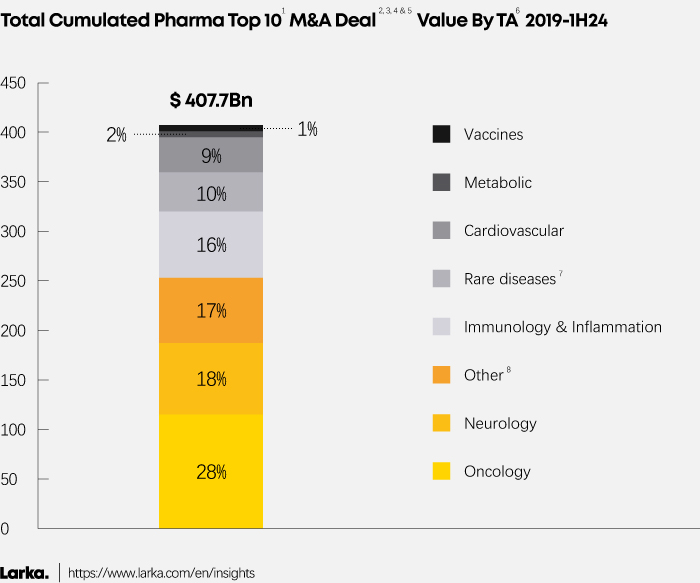

Overall, oncology market remained heavily prioritized despite uncertain years

Representing 28% of total M&A deal value recorded from 2019 to H1 2024 (Figure 1), oncology unsurprisingly remains Big Pharma’s favourite therapeutic area (TA) for dealmaking.

Among the most active acquirers in this area are Merck, with 7 out of 11 deals targeting oncology assets, Bristol-Myers Squibb (BMS) with 4 out of 6 deals—including three deals exceeding $4 billion—and Sanofi with 7 out of 10 deals [1].

Over the past five years, Pharma companies have consistently aimed at strengthening their oncology portfolios with innovative science, products, and platforms, as oncology remains the largest and fastest-growing market.

Figure 1

1. Top 10 Pharma based on Pharma sales for each year (excluding diagnostic, medical device, nutrition, etc.). 2023 Top 10 Pharma includes Pfizer, AbbVie, J&J, Novartis, Merck & Co, Roche, BMS, AstraZeneca, Sanofi and GSK vs. 2019 Top 10 Pharma includes Roche, Novartis, Pfizer, Merck & Co, Bayer, J&J, Sanofi, AbbVie, GSK and Takeda.

2. Deals closed/completed based on announcement in annual reports.

3. Deal value is the purchased price mentioned in annual reports.

4. M&A deals focusing on Pharma (excluding diagnostic, medical device, etc.).

5. Only M&A Buy-Out (excluding partial equity investment).

6. Amount allocated based on the pipeline of the acquired company.

7. Rare diseases only includes a part of Alexion & Shire's acquisitions.

8. Other—as TA—includes hematology, ophthalmology, fibrosis, etc.

This major focus in oncology is driven by unmet medical needs and the significant growth potential of the oncology market, which is fueled by a large patient population and rising cancer incidence. Historically, oncology has generated the most revenue for pharmaceutical companies, reinforcing its strategic importance and driving continuous investment and innovation in this field.

Looking ahead, investments in oncology are expected to continue. Oncology drugs will remain among the most profitable in the market and Pharma companies are looking for ways of securing growth to address upcoming revenue challenges.

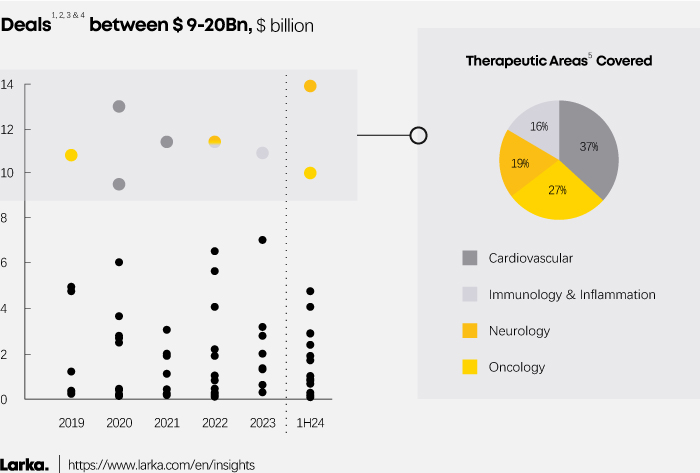

Momentary slowdown for large oncology deals amid the pandemic

During the 2020-2023 period, $9-$20 billion deals in oncology temporary slowed for Top 10 Pharma companies—which redirected their attention towards advanced clinical stage companies developing products in cardiovascular and immunology & inflammation areas (Figure 2-3).

This temporary shift could be a strategic reaction from Pharma companies as the pandemic emphasized the need to address underlying medical conditions such as cardiovascular diseases and immune disorders—which can be exacerbated by viral infections like Covid.

By 2023 a post-pandemic reversal began, signalling a return to normal with a renewed interest in oncology. Pfizer led the way by acquiring Seagen in 2023, followed by AbbVie’s recent acquisition of Immunogen [5].

Steady interest for smaller oncology deals targeting innovative technologies

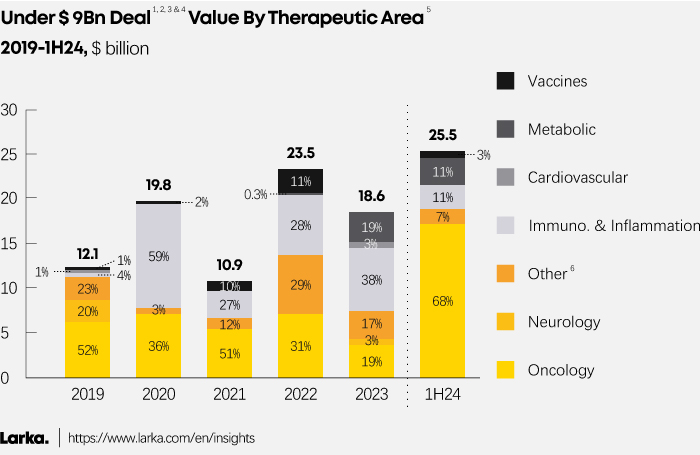

While $ 9-20Bn investments targeting late-stage oncology assets slowed temporarily (Figure 2), Big Pharma kept eyes on innovative immunology and oncology assets via under $9 billion acquisitions (Figure 6).

Indeed, interest in oncology-focused companies remained consistent during the pandemic. This continued interest despite global challenges highlights the critical importance and financial potential of the oncology market.

Figure 2-3

1. Deals closed/completed based on announcement in annual reports.

2. Deal value is the purchased price mentioned in annual reports.

3. M&A deals focusing on Pharma (excluding diagnostic, medical device, etc.).

4. Only M&A Buy-Out (excluding partial equity investment).

5. Amount allocated based on the pipeline of the acquired company.

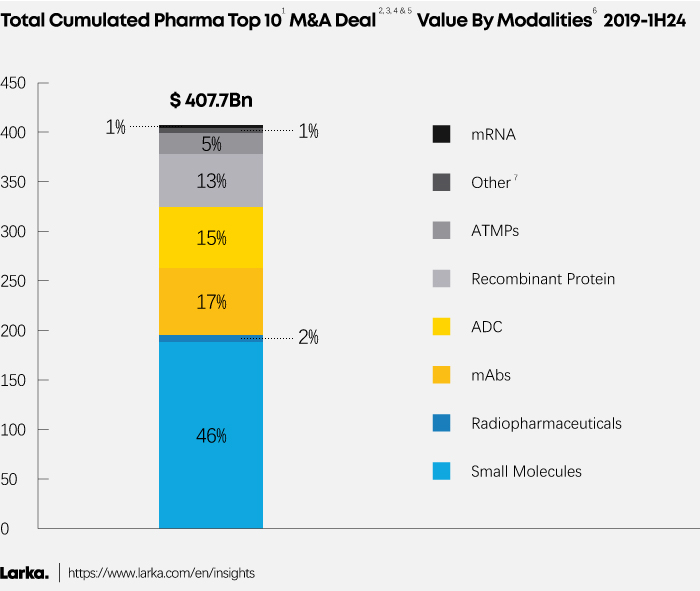

Small molecule (SM) drugs are still a major theme

Accounting for 46% of the acquisitions made by the Top 10 pharmaceutical companies, small molecules remained a key modality over the past five years despite the rise of biologics (Figure 4). Notably, BMS led this trend with 4 out of its 6 deals targeting companies focusing solely on SM drugs, followed by Novartis with 5 out of 8 deals [2].

Well-established and trusted by drugmakers, small molecules remain attractive as they address a wide range of TAs, including critical markets like oncology and neurology.

Additionally, the SM universe has seen the emergence of innovative technologies such as Proteolysis targeting chimeras (PROTACs) and other SM with complex structures that further enhance their potential and versatility.

LATEST INSIGHTS

Biotech Funding: Why ADCs Became VC Magnets in 2024

Antibodies are in vogue, especially antibody-drug conjugates

Antibody-based assets are the most attractive behind small molecules, representing more than a third of total M&A deals from 2019 to H1 2024 (Figure 4)—including 17% for monoclonal antibodies (mAbs) and 15% for antibody-drug conjugates (ADCs).

Figure 4

1. Top 10 Pharma based on Pharma sales for each year (excluding diagnostic, medical device, nutrition, etc.). 2023 Top 10 Pharma includes Pfizer, AbbVie, J&J, Novartis, Merck & Co, Roche, BMS, AstraZeneca, Sanofi and GSK vs. 2019 Top 10 Pharma includes Roche, Novartis, Pfizer, Merck & Co, Bayer, J&J, Sanofi, AbbVie, GSK and Takeda.

2. Deals closed/completed based on announcement in annual reports.

3. Deal value is the purchased price mentioned in annual reports.

4. M&A deals focusing on Pharma (excluding diagnostic, medical device, etc.).

5. Only M&A Buy-Out (excluding partial equity investment).

6. Amount allocated based on the pipeline of the acquired company.

7. Other—as modality—includes heparin derived and measles virus vector.

Monoclonal antibodies, a well-established modality

mAbs address key markets like oncology and immunology—and are also being developed to tackle a wide range of serious diseases.

Besides being a well-established modality in various TAs, the mAbs universe is also driving continuous innovation. The latest being bispecific antibodies, which are emerging as a new class of biologics and showing great therapeutic potential.

These strong incentives to keep investing in the mAbs universe have been reflected in Big Pharma’s M&A strategies. Over the past five years, every 2024 Top 10 Pharma companies have acquired at least one target developing monoclonal antibodies.

Antibody-drug conjugates field is booming

Big Pharma's interest for antibody-drug conjugates (ADCs) has sky-rocketed. With major acquisitions completed lately, the novel therapeutic modality has become a predominant theme. This surge is particularly striking given that there are currently 12 times more FDA-approved mAb-based drugs than ADCs on the market.

Notable deals recorded recently include Pfizer's megadeal with Seagen for $43.4 billion in 2023; AbbVie’s acquisition of Immunogen in Q1 2024 for approximately $10 billion and Ambrx acquisition by J&J in Q1 2024 for around $2 billion [3].

This growing appetite for ADCs is driven by three key attributes of the modality, which have helped foster an active market around this universe:

- ADCs consistently demonstrate good efficacy and safety results across various cancer types.

- ADCs avoid the complex patient administration and supply-chain challenges associated with other modalities like CAR-T.

- ADC assets are expanded beyond their initial focus in oncology to other TAs like immune system, dermatological or gastrointestinal diseases—ultimately increasing commercial opportunities.

The increased volume of dealmaking reflects the potential of ADC as a targeted cancer therapy—and investments are expected to carry on as the modality continues to build up clinical and commercial acceptance.

Key themes emerged amid the pandemic

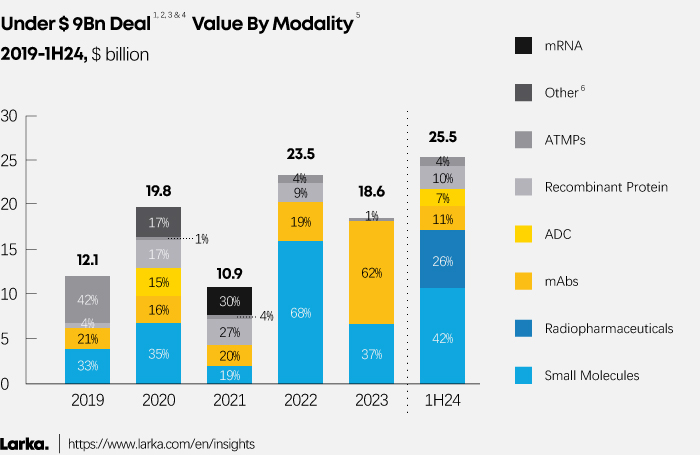

Vaccines and mRNA

During the pandemic vaccines and mRNA emerged as predominant themes, with vaccines representing 10% and 11% of under $ 9Bn deals in 2021 and 2022, versus less than 1% pre-pandemic (Figure 6). Simultaneously, mRNA emerged to represent 30% of total deal value in 2021 (Figure 5).

Figure 5

1. Deals closed/completed based on announcement in annual reports.

2. Deal value is the purchased price mentioned in annual reports.

3. M&A deals focusing on Pharma (excluding diagnostic, medical device, etc.).

4. Only M&A Buy-Out (excluding partial equity investment).

5. Amount allocated based on the pipeline of the acquired company.

6. Other—as modality—includes heparin derived and measles virus vector.

A shift of focus and resources towards vaccines and mRNA driven by several factors:

The pandemic highlighted the effectiveness and scalability of mRNA technology in vaccines, faster development and production timelines, and its potential to address a broad range of medical challenges beyond infectious diseases.

Key features that prompted deals such as Sanofi’s acquisition of Translate Bio in 2021—with the aim to enhance mRNA technology for vaccines and therapeutics, targeting areas like immunology, oncology, and rare diseases.

The development of novel platforms, such as the Multiple Antigen Presenting System (MAPS), also spurred significant industry interest. This disruptive technology led to GSK's acquisition of Affinivax for $2.2 billion in 2022 [6], underscoring the industry's commitment to advancing vaccine development.

Immunology and inflammation

M&A activity in immunology and inflammation surged between 2020 and 2023, driven by the heightened awareness of the immune system's critical role, particularly as severe COVID-19 outcomes were more pronounced in individuals with compromised immune responses. This has underscored the urgency of advancing therapeutic approaches targeting immune system deficiencies and external threats.

Figure 6

1. Deals closed/completed based on announcement in annual reports.

2. Deal value is the purchased price mentioned in annual reports.

3. M&A deals focusing on Pharma (excluding diagnostic, medical device, etc.).

4. Only M&A Buy-Out (excluding partial equity investment).

5. Amount allocated based on the pipeline of the acquired company.

6. Other—as TA—includes hematology, ophthalmology, fibrosis, etc.

Metabolic disease: a growing appetite for GLP-1

Interest in metabolic disease dramatically increased, with M&A investments in this area accounting for 19% of total deal value in 2023, versus 0.3% in 2022. A trend confirmed in the first half of 2024, with a share reaching 11% (Figure 6).

The metabolic disease area is on a roll, driven by its growth potential and high unmet needs. GLP-1 receptor agonists are emerging as a disruptive technology on the market, with clinical trial data increasingly validating their effectiveness in managing obesity and improving cardiovascular and metabolic health.

These promising prospects are reflected in recent M&A activity like Roche and Sanofi’s acquisition of Carmot Therapeutics for $2.9 billion in Q1 2024 and Provention Bio for $2.8 billion in 2023 [7]—and are expected to continue in the coming years.

Radiopharmaceuticals on the rise in H1 2024

While still a relatively young modality, with the first approvals dating back to 2018, radiopharmaceuticals has really built traction in the market of late.

Two deals were completed in the first half of 2024 with BMS acquisition of RayzeBio for $4.1 billion, and AstraZeneca acquiring Fusion Pharmaceuticals for $2.4 billion—and another deal announced by Novartis, which should acquire Mariana Oncology for approximately $1 billion [8].

With both completed transaction focusing on the oncology market, these 2 deals align with the ongoing surge in oncology (Figure 6)—as radiopharmaceuticals have become an attractive alternative to traditional radiation therapy for treating certain cancers.

REPORT'S METHODOLOGY

To analyze the M&A activities of each year’s Pharma Top 10, we have combined a dot plot analysis with an algorithm designed to measure the minimal distance between deal values.

This approach enabled us to determine 3 distinct clusters, based on deal sizes and strategic focus.

- Megadeals (above $20 billion): These transactions involve large pharmaceutical companies acquiring firms with significant commercial assets across multiple indications. Such deals typically focus on expanding the acquirer’s therapeutic portfolio and strengthening its position in key markets.

- Deals between $9 billion and $20 billion: This category includes deals where the target companies possess late-stage clinical assets and a limited number of commercial products. These acquisitions aim to reinforce the buyer’s pipeline with near-market candidates and consolidate assets across select therapeutic areas.

- Deals below $9 billion: Smaller acquisitions generally target companies with a narrow focus on one or two modalities. These transactions are driven by the strategic need to access innovative platforms or technologies that can complement the acquirer’s existing capabilities.

By categorizing M&A activities into these three groups, we provide a clearer understanding of the strategic priorities and investment patterns of top pharmaceutical companies, reflecting their approach to building long-term value and achieving sustainable growth.

RELATED INSIGHTS

Top 10 Pharma: M&A Trends and Outlook for 2024