Antibody-Drug Conjugates (ADC)-focused biotech companies have surged back into the spotlight in 2024, attracting significant venture capital (VC) funding values and volumes.

KEY TAKEAWAYS

- VC funding in ADC-focused biotech surged in 2024, with deal value and volume rebounding sharply and its share more than doubling compared to the 2020-2023 period.

- Nearly 20% of VC funding in oncology now goes to antibody-drug conjugates (ADCs)—reflecting their strong efficacy, safety, and transformative potential in cancer treatment.

- Venture capitalists are shifting focus from later-stage to early-stage ADC biotech, reflecting growing investor confidence in their transformative potential.

- ADC biotech funding in Europe mirrors North America’s dynamics but remains smaller in scale due to less market maturity, fewer biotech hubs, and a more cautious investment culture.

ADC Biotech Funding Roared Back in 2024

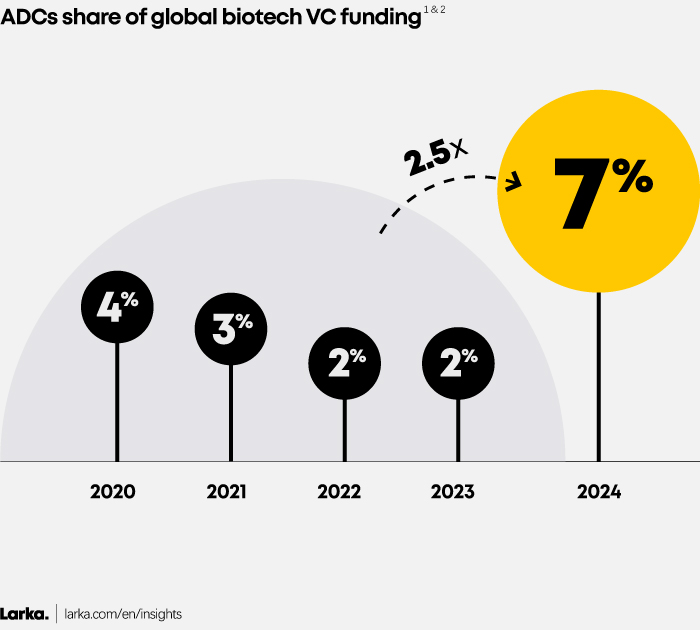

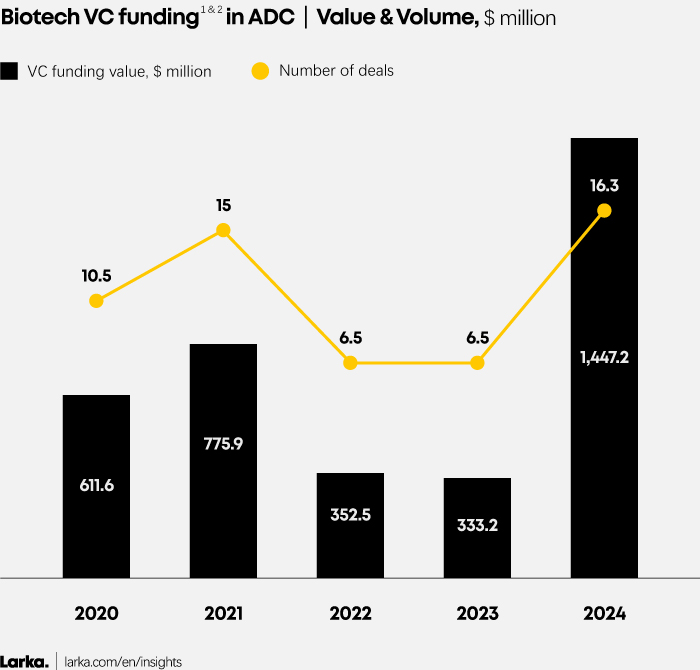

Biotech VC funding in ADCs has made a thunderous comeback in 2024. Deal value and volume surged after two years of decline in 2022 and 2023 (Figure 2), while the ADC share of total biotech VC funding has more than doubled compared to the 2020-2023 period (Figure 1).

Figure 1

1. VC funding focusing on Pharma (excluding diagnostic, medical device, etc.).

2. The value allocation by modality has been calculated by dividing the total funding amount ($) for a biotech company by the number of modalities present in its pipeline. Similarly, the volume allocation by modality has been calculated by dividing a single deal (since one deal corresponds to one biotech) by the number of modalities in that pipeline.

1. VC funding focusing on Pharma (excluding diagnostic, medical device, etc.).

2. The value allocation by modality has been calculated by dividing the total funding amount ($) for a biotech company by the number of modalities present in its pipeline. Similarly, the volume allocation by modality has been calculated by dividing a single deal (since one deal corresponds to one biotech) by the number of modalities in that pipeline.

This resurgence comes after a challenging period marked by high inflation, elevated interest rates, and geopolitical instability. Faced with these hurdles, VCs grew more cautious—focusing on existing portfolios while becoming highly selective with new investments.

However in 2024, venture capitalists renewed their confidence in ADC-focused biotech—and we have identified 5 key factors that are driving this significant surge:

Technological advancements

Established manufacturing processes and recent innovations in linkers, payloads, and monoclonal antibodies (mAbs) have greatly enhanced the efficacy and safety profiles of ADCs. These advancements have also lowered production costs, mitigating risks for venture capital investors.

Strong clinical performance

ADCs have demonstrated significant success in clinical trials and regulatory approvals, confirming their viability and boosting investor confidence.

Since the first ADC, Mylotarg® (gemtuzumab ozogamicin), was approved by the FDA in 2000, 13 ADCs have gained market approval worldwide—including the latest to date, AbbVie’s ELAHERE® (mirvetuximab soravtansine), which received its first EU approval in 2024.

Supportive regulatory environment

Accelerated approval processes and favourable regulatory frameworks have reduced development timelines and costs, making investments in ADCs more appealing to venture capital funds.

Pharma collaboration and M&A

Strategic partnerships and acquisitions by leading pharmaceutical companies highlight the therapeutic promise of ADCs, attracting greater interest from venture capital investors. A notable example is Pfizer's acquisition of Seagen for $43.4 billion in 2023, which underscores the immense value and potential of ADC technology.

Market Potential and Financial Gains

The robust market potential and high return on investment associated with successful ADC products, combined with active pharma M&A, make them exceptionally attractive to venture capital funds.

How Antibody-Drug Conjugates Are Changing Cancer Treatment

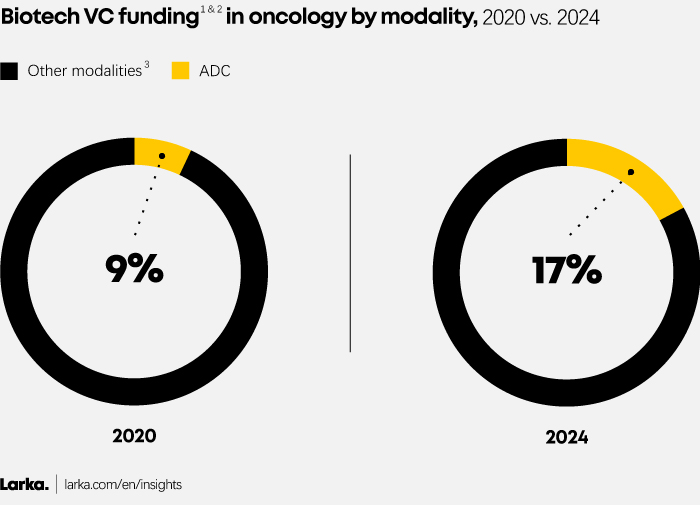

Another reason healthcare venture capitalists are drawn to ADCs is because they address oncology, a major therapeutic area with a huge potential market.

Demonstrating strong efficacy and safety results across various cancer types, ADCs now attract almost 20% of all VC funding in oncology (Figure 3).

Figure 3

1. VC funding focusing on Pharma (excluding diagnostic, medical device, etc.).

2. The value allocation by modality has been calculated by dividing the total funding amount ($) for a biotech company by the number of modalities present in its pipeline. Similarly, the volume allocation by modality has been calculated by dividing a single deal (since one deal corresponds to one biotech) by the number of modalities in that pipeline.

3. Others modalities include small molecules, large molecules and ATMPs.

What Are Antibody-Drug Conjugates?

Antibody-drug conjugates are an innovative class of targeted therapies designed to deliver potent cytotoxic drugs directly to cancer cells. Each ADC therapy is composed of three key components: a monoclonal antibody (mAb) that recognizes and binds to specific cancer cell markers, a cytotoxic drug that kills the targeted cells, and a chemical linker that ensures the precise release of the drug to the intended site.

What Do ADCs Target?

ADCs target specific antigens expressed on the surface of cancer cells, minimizing damage to healthy cells. By combining the selectivity of mAbs with the potency of cytotoxic drugs, ADCs offer a highly targeted approach to cancer treatment, reducing systemic toxicity and improving therapeutic efficacy.

"Innovation in ADC technology, particularly in bioconjugation with continued progress in linker chemistry, is enhancing the potential to reduce off-target effects and expand therapeutic options—establishing ADCs as a vital component in the evolution of cancer treatment."

Olivier Dumortier, PhD | Subject Matter Expert at Larka

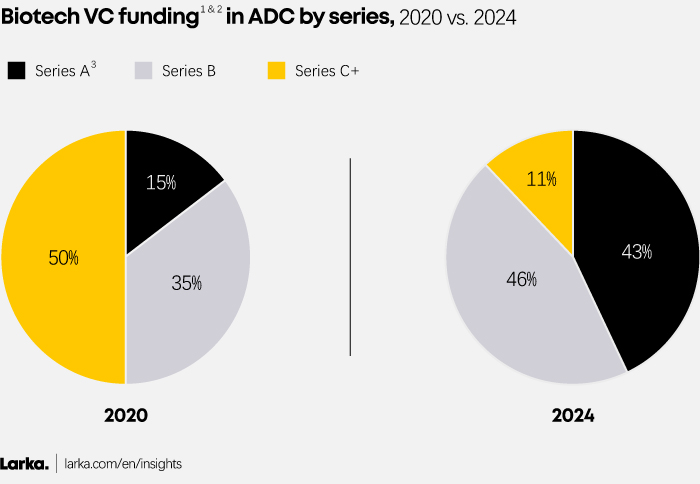

Investor Confidence is Boosting Early-Stage Biotech Funding

Venture capital confidence in ADC-focused biotech is reaching new heights, signalling a shift in investment strategies over the past few years.

Figure 4

1. VC funding focusing on Pharma (excluding diagnostic, medical device, etc.).

2. The value allocation by modality has been calculated by dividing the total funding amount ($) for a biotech company by the number of modalities present in its pipeline. Similarly, the volume allocation by modality has been calculated by dividing a single deal (since one deal corresponds to one biotech) by the number of modalities in that pipeline.

3. Series A include Series Seed.

In 2020, VC funds predominantly targeted later-stage biotech companies, prioritizing those with mature pipelines and proven clinical potential. This cautious approach reflected a preference for minimizing risks by backing established players in the space.

By 2024, the landscape has noticeably evolved, with VCs channelling resources into earlier-stage biotech companies raising Series A funding rounds (Figure 4). This willingness to support startups that have yet to achieve clinical milestones highlights a significant boost in investor confidence in ADCs transformative potential.

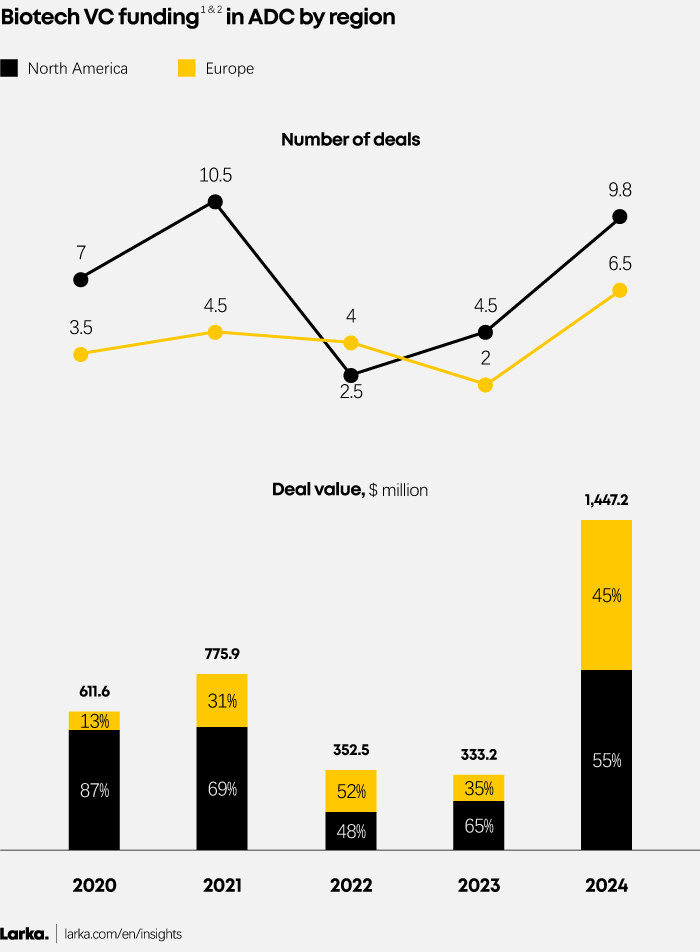

EU vs. NA Funding: Same dynamics overall, but smaller scale in Europe

Figure 5

1. VC funding focusing on Pharma (excluding diagnostic, medical device, etc.).

2. The value allocation by modality has been calculated by dividing the total funding amount ($) for a biotech company by the number of modalities present in its pipeline. Similarly, the volume allocation by modality has been calculated by dividing a single deal (since one deal corresponds to one biotech) by the number of modalities in that pipeline.

The funding landscape for ADC biotech shows comparable dynamics across Europe and North America, but the scale of activity in the two regions remains different for three key reasons:

Market Maturity and Size

North America leads the ADC biotech sector with a more mature market and larger scale, supported by well-established infrastructure. Major biotech hubs and leading research institutions foster a robust ecosystem of investors, academics, and industry leaders, driving significant funding activity.

In contrast, Europe’s ADC market is smaller and less mature, with fewer concentrated biotech hubs leading to lower and more dispersed investment levels. However, the region is catching up, as funding gradually increases alongside market development and growing investor confidence.

Corporate and Strategic Acquisitions

In North America, large pharmaceutical companies actively drive the ADC biotech space through high-profile acquisitions and partnerships. Notable transactions include Pfizer's acquisition of Seagen for $43.4 billion in 2023, AbbVie’s acquisition of ImmunoGen for $10 billion in 2024, and Johnson & Johnson’s acquisition of Ambrx for $2 billion in 2024. These deals validate the transformative potential of ADC technologies and significantly boost venture capital interest.

Cultural and Economic Factors

North America’s entrepreneurial and risk-taking culture fuels higher and more dynamic funding levels in innovative technologies like ADCs. This approach drives substantial investments and accelerates the region’s leadership in the sector.

Europe, while traditionally more cautious about emerging technologies, is increasingly focusing on ADCs as investor interest grows. The spotlight on ADC biotech in Europe reflects the sector’s potential to drive transformative advancements, even within a more conservative investment culture.

MORE PHARMA INSIGHTS